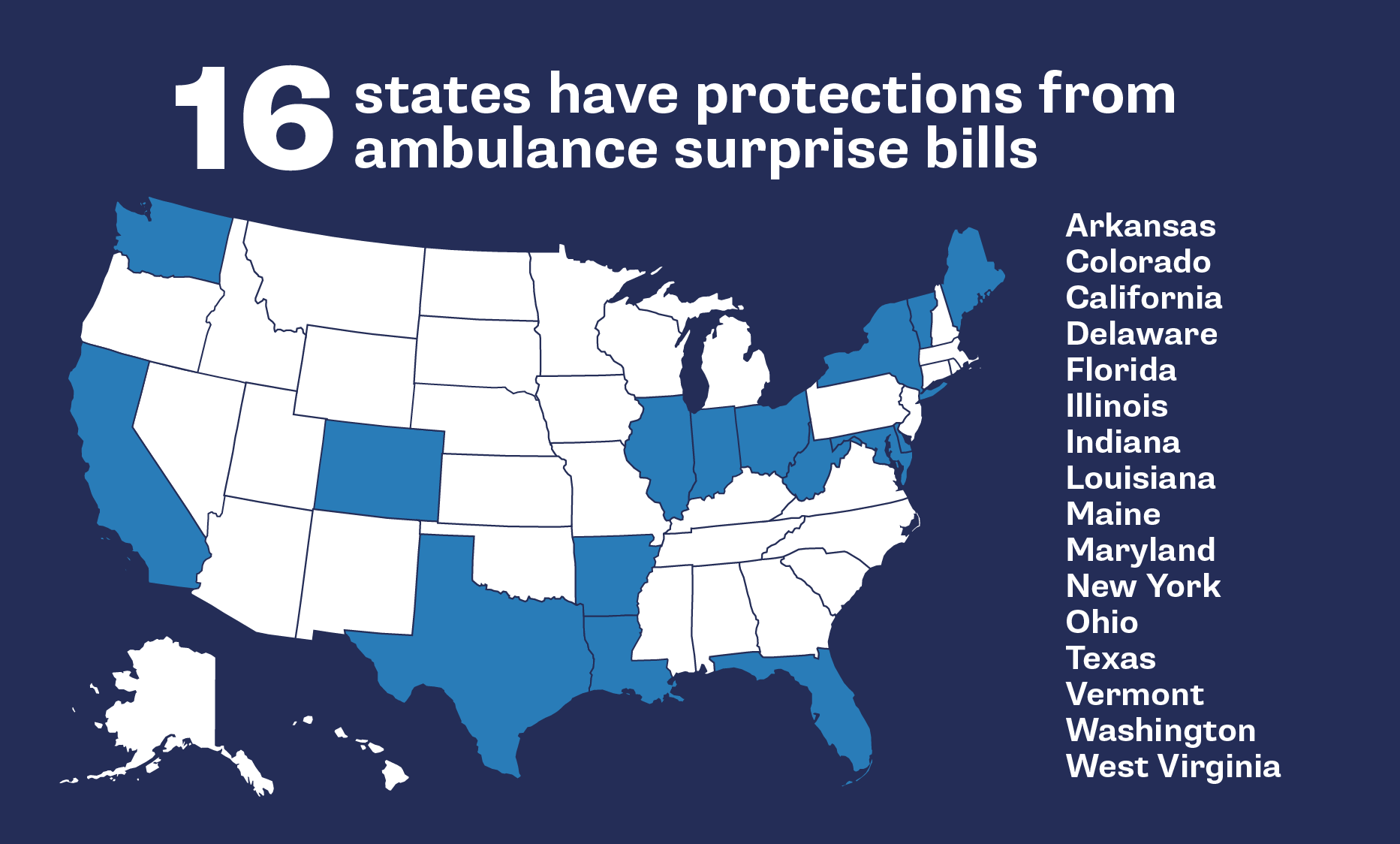

Tell your U.S. senators: Pass health care price transparency

We need hospital prices before we receive care to end medical billing that unnecessarily drives up our costs.

Medical debt negatively impacts the credit scores of millions of Americans. This problem is so prevalent that one in five Americans had a medical bill they could not pay at the time they received care. Those bills often end up in debt collections, and then show up on a person’s credit report. In 2021, 43 million credit reports listed medical debts in collection.

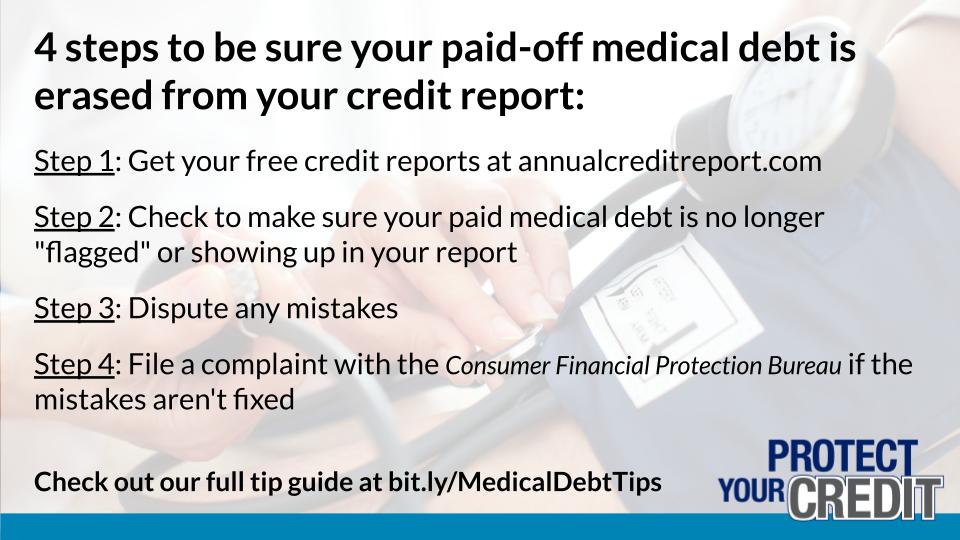

U.S. PIRG Education Fund released a tip sheet that Americans can use to ensure any paid medical debt has been removed from their credit reports. The tips explain how to obtain a free copy of credit reports, where to check to make sure paid medical debt has been removed, and how to dispute any mistakes in a credit report.

Until now, medical debt, even when it is paid off, remained on a credit report for up to seven years. But a new policy voluntarily announced in March by the three major credit bureaus — Equifax, Experian and TransUnion — changes how paid medical debt will be reported on credit reports starting on July 1.

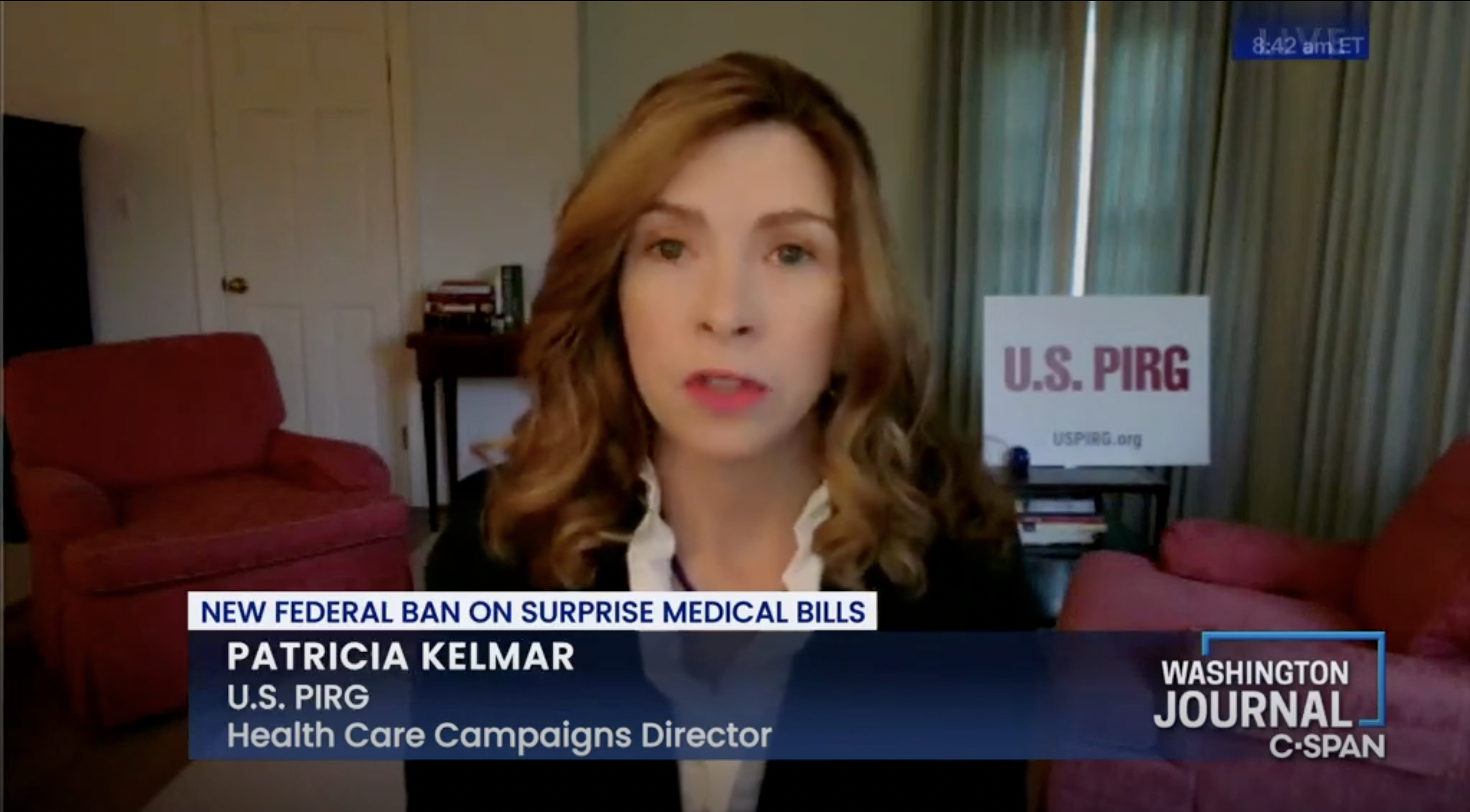

“It’s incredible to think that even when you pay off your medical debt, the credit bureaus continue to penalize Americans by lowering their credit scores,” said Patricia Kelmar, U.S. PIRG Education Fund’s health care campaigns director. “Consumers have been denied auto loans, credit cards and mortgages — and low credit scores can even impact hiring decisions by potential employers.”

The three promised changes include:

As of July 1, paid medical debt will be erased from credit reports

New medical debt won’t be included in credit reports until a year after the debt is given over to collection agencies, rather than the current six months.

Beginning in 2023, credit reports will not include medical debt of less than $500

We need hospital prices before we receive care to end medical billing that unnecessarily drives up our costs.

Energy Conservation & Efficiency

Energy Conservation & Efficiency