The CFPB’s Public Consumer Complaints Database Gets Real Results for Credit Card Holders

Maryland PIRG Foundation

Addendum: After publication of this report, it came to our attention that the dataset we used to approximate the size of credit card companies relative to each other—‘purchase volume’—was incomplete. The dataset omitted information on certain cards that companies issue on behalf of other entities, such as the cards GE Capital Retail issues on behalf of some department stores. This omission affects several companies, and would tend to increase those companies’ complaint rates relative to companies that are less involved in such arrangements (see chart on p. 15). Although we are unable to verify this information, a representative from GE Capital has stated that a more complete figure for their total purchase volume would change their complaints per billion dollars in purchase volume from 88 to 17 or 18, placing them in the middle of the rankings rather than at the top.

Executive Summary

The Consumer Financial Protection Bureau (CFPB) was established in 2010 in the wake of the worst financial crisis in decades. Its mission is to identify dangerous and unfair financial practices, to educate consumers about these practices, and to regulate the financial institutions that perpetuate them.

To help accomplish these goals, the CFPB has created and made available to the public the Consumer Complaint Database. The database tracks complaints made by consumers to the CFPB and how they are resolved. The Consumer Complaint Database enables the CFPB to identify financial practices that threaten to harm consumers and enables the public to evaluate both the performance of the financial industry and of the CFPB.

This is the fourth in a series of reports that review complaints to the CFPB nationally and on a state-by-state level. In this report we explore consumer complaints about credit cards with the aim of uncovering patterns in the problems consumers are experiencing with their credit cards and documenting the role of the CFPB in helping consumers successfully resolve their complaints.

Despite the benefits to consumers brought by enactment of the Credit Card Accountability Responsibility and Disclosure (Credit CARD) Act of 2009, consumer complaints about credit cards remain common. Between November 2011 – when the Consumer Financial Protection Bureau began recording data on credit cards – and September 10th, 2013, the CFPB recorded more than 25,000 complaints about credit cards.

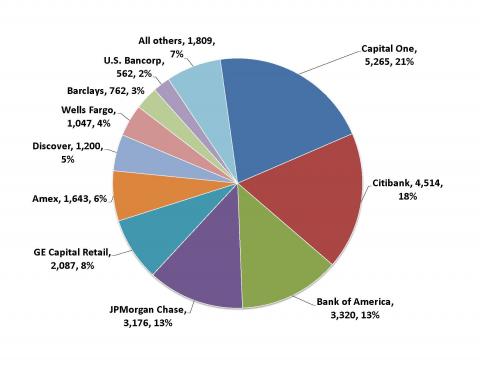

- Capital One was the most complained-about credit card issuer by total number of complaints, followed by Citibank, Bank of America and JPMorgan Chase.

- GE Capital Retail was the most complained-about credit card company among the top 10 card issuers based on the ratio of complaints to card purchase volume. GE Capital Retail experienced 88 complaints per billion dollars in purchase volume, followed by Capital One with 46 complaints and Barclays with 25 complaints per billion dollars in purchase volume.

- Ten U.S. credit card companies accounted for about 93 percent of all consumer complaints to the CFPB. (See Figure ES-1.)

Figure ES-1. Ten Companies Accounted for About 93 Percent of Complaints to the CFPB about Credit Cards

Consumers face a wide array of problems with their credit cards. The most common problem faced by consumers was billing disputes, followed by difficulties with annual percentage rates (APR) or interest rates, and trouble with identity theft, fraud or embezzlement. Thousands of consumers also complained about problems with closing or canceling accounts, late fees and collection practices.

Figure ES-2. Billing Disputes Are the Most Frequent Source of Complaints to the CFPB about Credit Cards

Complaints about companies vary by state, and state residents vary in their tendency to reach out to the CFPB.

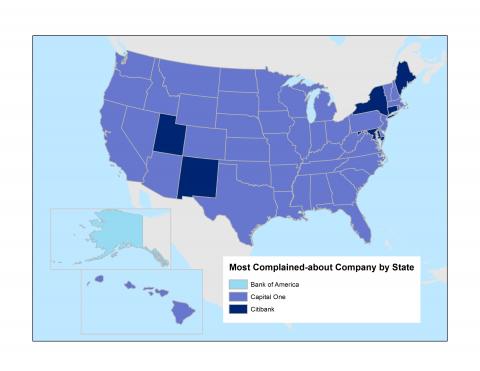

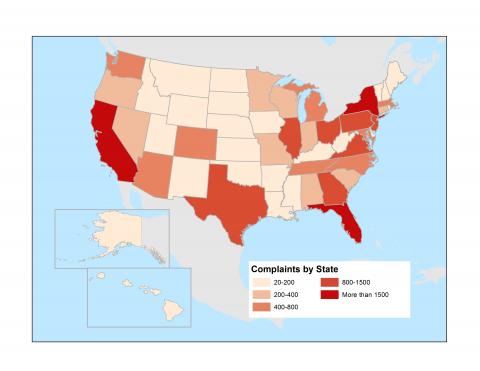

- Capital One was the most complained-about credit card company in 43 states, while Citibank was the most complained-about company in six states and the District of Columbia. Bank of America was the most complained-about company in Alaska. (See Figure ES-3.)

- Residents of Northeastern states are most likely to complain about their credit cards, while consumers in the Midwest and South are least likely. The District of Columbia had the most complaints per capita, followed by Delaware, Maryland, New York, New Jersey, Florida, Connecticut, Massachusetts, Virginia and Maine.

Figure ES-3. Capital One Is the Most Complained-about Credit Card Company in 43 States

Figure ES-4. Complaints about Credit Cards Vary by State

The CFPB is making a significant difference for consumers facing difficulty with their credit card companies:

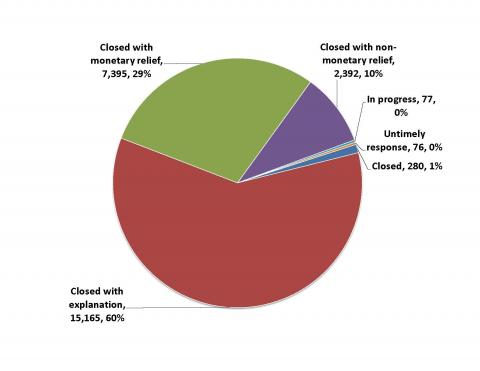

- The CFPB has helped more than 7,300 consumers – about three in 10 complainants – to receive monetary compensation as a result of their credit card complaints. (See Figure ES-5.) The median amount of monetary relief for consumers with credit card complaints through mid-2013 was $128. More than 2,000 additional consumers have had their complaints closed with some form of non-monetary relief, which includes actions such as altering account terms or fixing an incorrect submission of information to a credit bureau.

Figure ES-5. Nearly 40 Percent of Credit Card Customers Received Monetary or Non-Monetary Relief After Complaining to the CFPB

- Credit card companies vary greatly in the degree to which they respond to consumer complaints with offers of monetary relief. Nearly two out of every five complaints concerning GE Capital Retail resulted in monetary relief to the consumer, while only about 20 percent of complaints concerning American Express did.

- About 20 percent of responses from credit card companies were deemed unsatisfactory by consumers and were subjected to further dispute.

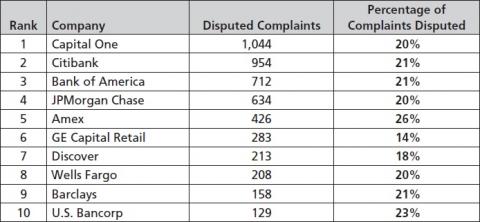

- Of the 10 companies with the most overall complaints, the company with the highest number of disputed responses was Capital One, with 1,044, followed by Citibank and Bank of America. (See Table ES-1.) These three credit card companies were also the three companies with the highest number of overall complaints.

Table ES-1. Companies Vary in the Degree to which Consumers Dispute their Responses to CFPB Complaints

- Of the 10 companies with the most overall complaints, the company with the greatest proportion of disputed responses was American Express (Amex), with just over a quarter of responses disputed. Of these same companies, GE Capital Retail had the lowest proportion of disputed responses, at 14 percent.

The Consumer Financial Protection Bureau’s Consumer Complaint Database is a key resource for consumer protection. To enhance the ability of the CFPB to respond to consumer complaints, the CFPB should:

- Add more detailed information to the database, such as actual complaint narratives, detailed complaint categories and subcategories, complaint resolution details, consumer dispute details, and data regarding membership in classes protected from discrimination by law. Expansion of complaint-level details should include more information about amounts and types of monetary and non-monetary relief. Software and other techniques should be used to protect consumer privacy by giving consumers the right not to provide details and by taking steps to prevent the release of personally-identifiable information or the re-identification of consumers. It is critical that the Bureau achieve the disclosure of more individual complaint details while simultaneously making every reasonable effort to protect personal data.

- Add features such as clear definitions of terms and instructions.

- Provide regular trend analyses and monthly detailed reports on complaint resolutions and disputes.

- Simplify the interfaces that allow users to summarize complaint database reports in graphical and printable formats.

- Publicize information about the CFPB complaints process in forums that are likely to be seen by credit card users. The agency should develop more outreach mechanisms for consumer education about the database and its services for consumers, including through the creation of educational materials to be distributed on- and off-line, through more events outside Washington, D.C., and through non-profit organizations.

- Develop free applications (apps) for consumers to download to smartphones to access information about how to complain about a firm and how to review complaints in the database.

- Expand the Consumer Complaint Database to include discrete complaint categories for high-cost credit products such as auto title loans and prepaid cards. We commend the CFPB for adding payday loan complaints to the database in November 2013.

- Continue to use the information gathered from the Consumer Complaint Database, from supervisory and examination findings, and from other sources to require a high, uniform level of consumer protection and ensure that responsible industry players can better compete with those who are using harmful practices.