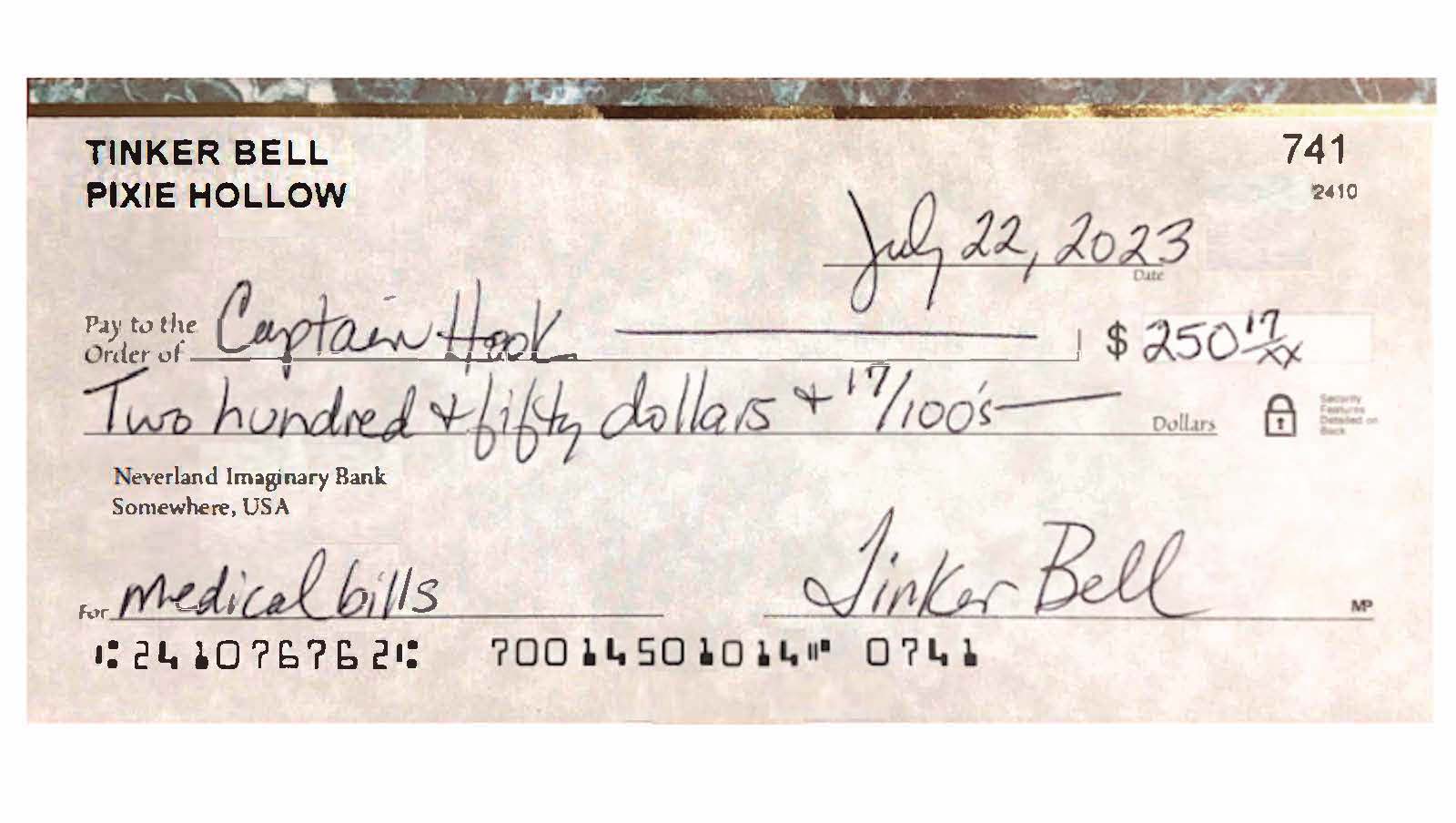

Checks are easy to complete, but it's important to do it carefully

People don’t rely on checks as much as they did in the 1990s, but checks still are needed from time to time and you should know how to fill one out if you have a checking account.

It’s important to realize that a check is a legal document. If you give a check to someone, you’re saying you agree to pay them this much money. You should fill checks out carefully and also protect your blank checks. They can be stolen and written out to someone and cashed, even without your actual signature. Yes, you generally can get your money back if this happens, but it can take weeks, and there’s no guarantee.

You can order checks through your bank or third-party companies. No matter what, you should make sure the company is a member of the Check Payment Systems Association or complies with the security features that checks must have, such as watermarks.

Always use a pen, not pencil. You may opt for a gel pen that makes it more difficult for someone to alter the check with rubbing alcohol or fingernail polish.

Always keep a record of checks you write, along with other payments, so you don’t overdraw your account. You can use Excel or any spreadsheet, an old-fashioned checkbook ledger or a phone app, such as Balance My Checkbook by LingsDesigns (a favorite of mine). Whatever system that you’ll use and keep up with is great.

Remember that a check provides proof that you paid someone. If there’s a question later about whether a bill or debt was paid, the bank can provide you with documentation.

Review your account activity at least once a week to check off what has cleared and make sure that all transactions match the amount you thought they were.

Consumer Watchdog, U.S. PIRG Education Fund

Teresa directs the Consumer Watchdog office, which looks out for consumers’ health, safety and financial security. Previously, she worked as a journalist covering consumer issues and personal finance for two decades for Ohio’s largest daily newspaper. She received dozens of state and national journalism awards, including Best Columnist in Ohio, a National Headliner Award for coverage of the 2008-09 financial crisis, and a journalism public service award for exposing improper billing practices by Verizon that affected 15 million customers nationwide. Teresa and her husband live in Greater Cleveland and have two sons. She enjoys biking, house projects and music, and serves on her church missions team and stewardship board.