The high cost of health care imposes a steep burden on Oregon consumers. Expensive monthly insurance premiums, high deductibles, and expenses not covered by insurance all add to the strain on Oregonians’ finances, leaving them more vulnerable to other financial problems. This report describes the onerous fiscal toll health care costs impose on Oregonians – as observed in bankruptcy data – and identifies policies to help reduce the high cost of care, including implementation of a public option health plan.

The analysis in this report is based on nearly 8,000 Chapter 7 and Chapter 13 bankruptcy filings in Oregon in 2019. These filings contained detailed information about each consumer’s income, debts and creditors. Bankruptcy filings do not reveal why a consumer decided to file for bankruptcy or whether a consumer had health insurance, but they nonetheless permit a detailed analysis of medical debts.

One indication of the financial burden of health care is the number of Oregonians filing for bankruptcy who report having medical debt. In 2019, at least 60% of Chapter 7 and Chapter 13 bankruptcy filings in Oregon included medical debt.

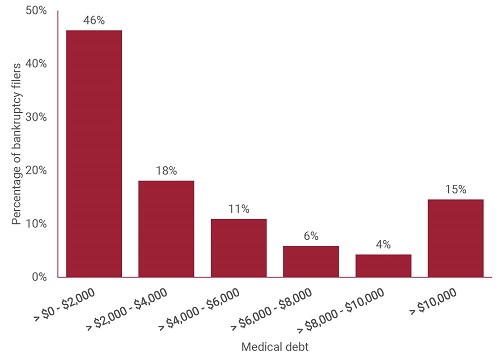

Many bankruptcy filers reported having large amounts of medical debt. Of bankruptcy filers who had medical debt, more than 600 (15%) reported having over $10,000 of medical debt.

- The median medical debt among those with medical debt was $2,326.

- Two bankruptcy filers reported more than $500,000 of medical debt.

Figure ES-1. Distribution of medical debt levels (among filers with medical debt)

Note: Excludes bankruptcy filers who indicated having medical debt but listed the amount as $0.

Medical debt affected bankruptcy filers at all income levels. In some cases, bankruptcy filers reported total debt that exceeded their annual income.

- The median annual income of filers who reported medical debt was $36,530, but in each income bracket below $100,000 per year the majority of filers had medical debt.

- 155 bankruptcy filers (3% of filers with medical debt) reported medical debt that was more than their annual income. Approximately 2,300 bankruptcy filers listed medical debts that totaled 5% or more of their annual income in the year they filed for bankruptcy.

Medical debt is a problem across the state. In every county where consumers filed for bankruptcy, they reported medical debt. In Oregon’s 10 most populous counties, the percentage of filers who had medical debt ranged from 52% to 69%, and the median amount of debt ranged from $1,723 to $3,664. In general, consumers in counties with a higher percentage of filers with medical debt also reported greater median amounts of debt. See Table ES-1.

Table ES-1. Bankruptcy filings for the 10 most populous Oregon counties

| Percent |

Rank |

Amount |

Rank |

| 1 |

Multnomah (Portland) |

1,223 |

52% |

10 |

$1,723 |

10 |

| 2 |

Washington (Hillsboro) |

1,079 |

59% |

8 |

$2,154 |

8 |

| 3 |

Clackamas (Lake Oswego) |

757 |

57% |

9 |

$2,260 |

6 |

| 4 |

Lane (Eugene) |

758 |

66% |

3 |

$2,976 |

4 |

| 5 |

Marion (Salem) |

956 |

60% |

6 (tie) |

$2,195 |

7 |

| 6 |

Jackson (Medford) |

414 |

62% |

5 |

$2,048 |

9 |

| 7 |

Deschutes (Bend) |

454 |

60% |

6 (tie) |

$3,142 |

3 |

| 8 |

Linn (Albany) |

353 |

69% |

1 |

$3,664 |

1 |

| 9 |

Douglas (Roseburg) |

204 |

67% |

2 |

$2,264 |

5 |

| 10 |

Yamhill (McMinnville) |

201 |

65% |

4 |

$3,400 |

2 |

Note: The calculation of the median debt excludes filers who indicated they had medical debt but listed the amount as $0.

Bankruptcy filers most often reported owing money to the issuer of a health care-specific credit card and to large networks of hospitals and health care providers.

- The single most frequently listed medical debt holder in Oregon was not a health care provider, but rather CareCredit from Synchrony Bank, a credit card for health care.

- Forty percent of medical debt could be attributed to the 10 health care networks that were most frequently listed in bankruptcy filings. Health care networks are large hospital systems and their affiliated providers.

One reason so many consumers filing for bankruptcy in Oregon have medical debt is that both health care and health insurance are expensive. Paying for insurance can strain household budgets, leaving consumers on shakier financial ground if they face an unexpected expense, medical or otherwise.

- Health care spending in Oregon in 2018 totaled $30.7 billion, more than $7,300 per person.

- Health insurance is expensive. Oregonians who buy insurance through the individual insurance market faced an average monthly premium for a benchmark plan of $443 in 2019, before subsidies. Employees with family coverage through an employer paid a monthly average of $450 toward their insurance premiums in 2019.

- In light of these costs, some Oregonians may forgo buying insurance. Six percent of Oregonians lacked health insurance in 2019.

Having health insurance does not fully protect Oregon consumers from additional health care expenses.

- As of 2016, nearly half of Oregonians who received insurance through their employer had high-deductible plans that required them to pay significant amounts before insurance began to cover medical expenses. On average, Oregonians have the third-highest deductibles in the nation, averaging nearly $4,000.

- A national study conducted in 2019 by the Kaiser Family Foundation found that one-third of all insured adults had difficulty affording their deductibles, and over half of those on the highest deductible plans lacked adequate personal savings to pay off their deductibles.

- When consumers have trouble paying medical bills, they may take on debt or spend down their savings, leaving them financially vulnerable. A recent poll found that the more than one-third of Oregonians who struggled to pay recent medical bills used strategies to cover their expenses that could leave them vulnerable, including using up most or all of their savings, borrowing money or getting another mortgage, and taking on large amounts of credit card debt.

To help consumers, Oregon policymakers should pursue a variety of policies to reduce the high cost of health care.

- Oregon should implement a public option health plan that lowers costs by reducing insurance premiums and other out-of-pocket expenses. The state recently passed a bill directing the Oregon Health Authority and the Department of Consumer and Business Services to design a public option plan, and to submit any legislative changes for approval in 2022. There are a variety of ways to lower costs with a public option, including having the state set provider reimbursement rates within the public option, or instituting a fixed payment to providers for each public option patient they care for. A study of how a public option might be structured in Oregon found that it could offer lower insurance premiums, and a national analysis found that a public health insurance option could reduce provider prices and increase competition in the insurance market.

- To slow the growth in health care costs, Oregon has adopted a health care cost growth target for all providers and insurers. The state should craft strong rules to enact its recently passed accountability mechanisms for the growth target. Performance improvement plans and financial penalties will only be effective if they are meaningful and enforced.

- The calculation of the median debt excludes bankruptcy filers who indicated they had medical debt but listed the amount as $0. Bankruptcy filers may do this if their debt has been sent to a collection agency, but they nonetheless want a specific creditor notified that they are seeking bankruptcy protection.

- Excludes 72 bankruptcy filers who had medical debt but listed $0 in annual income.

- The calculation of the median debt excludes bankruptcy filers who indicated they had medical debt but listed the amount as $0.

- Synchrony Bank, About CareCredit, archived on 10 April 2021 at http://web.archive.org/web/20210410221936/https://www.carecredit.com/about/.

- Liz Hamel, Cailey Muñana and Mollyann Brodie, Kaiser Family Foundation, Kaiser Family Foundation/LA Times Survey of Adults with Employer-Sponsored Health Insurance, May 2019, archived at http://web.archive.org/web/20201112031202/http://files.kff.org/attachment/Report-KFF-LA-Times-Survey-of-Adults-with-Employer-Sponsored-Health-Insurance; Liz Hamel, Mira Norton and Karen Pollitz et al., Kaiser Family Foundation, The Burden of Medical Debt: Results from the Kaiser Family Foundation/New York Times Medical Bills Survey, 5 January 2016, archived at http://web.archive.org/web/20201224100018/https://www.kff.org/report-section/the-burden-of-medical-debt-section-3-consequences-of-medical-bill-problems/; Craig Palosky and Sue Ducat, Kaiser Family Foundation, Benchmark Employer Survey Finds Average Family Premiums Now Top $20,000, 25 September 2019, archived at http://web.archive.org/web/20210204150530/https://www.kff.org/health-costs/press-release/benchmark-employer-survey-finds-average-family-premiums-now-top-20000/.

- Christian Wihtol, “State’s drive to cap health care spending kicks in next year,” The Lund Report, 19 August 2020, archived at http://web.archive.org/web/20200918110950/https://www.thelundreport.org/content/state%E2%80%99s-drive-cap-health-care-spending-kicks-next-year.

- Kaiser Family Foundation, Marketplace Average Benchmark Premiums, archived on 12 November 2020 at http://web.archive.org/web/20201112015041/https://www.kff.org/health-reform/state-indicator/marketplace-average-benchmark-premiums/?currentTimeframe=0.

- Annual premium divided by 12. Kaiser Family Foundation, Average Annual Family Premium per Enrolled Employee for Employer-Based Health Insurance, archived on 3 March 2021 at https://web.archive.org/web/20210307180044/https://www.kff.org/other/state-indicator/family-coverage/?currentTimeframe=0.

- Oregon Health Authority, Oregon Health Insurance Survey, accessed 20 April 2021 at https://visual-data.dhsoha.state.or.us/t/OHA/views/OregonUninsuranceRates/Uninsurance?%3Aiid=2&%3AisGuestRedirectFromVizportal=y&%3Aembed=y.

- Dana Tims, “Insurance guide 2018: Oregonians flock to high deductible health plans,” OregonLive, updated 9 January 2019, archived at https://web.archive.org/web/20210421002053/https://www.oregonlive.com/business/2017/10/insurance_guide_2018_high_dedu.html.

- Patrick Allen, Director, Oregon Health Authority, SB 889: Sustainable Health Care Cost Growth Target, Presentation to House Interim Committee on Health Care, 19 November 2018, archived at https://web.archive.org/web/20210423000551/https://olis.oregonlegislature.gov/liz/2019I1/Downloads/CommitteeMeetingDocument/207754.

- Ashley Kirzinger, Cailey Muñana, Bryan Wu and Mollyann Brodie, Kaiser Family Foundation, Data Note: Americans’ Challenges with Health Care Costs, 11 June 2019, archived at http://web.archive.org/web/20210227142107/https://www.kff.org/health-costs/issue-brief/data-note-americans-challenges-health-care-costs/.

- Todd Trierweiler, personal communication, 2 July 2021.

- Altarum, Oregon Residents Struggle to Afford High Healthcare Costs; COVID Fears Add to Support for a Range of Government Solutions Across Party Lines, Data Brief No. 91, June 2021, available at https://www.healthcarevaluehub.org/advocate-resources/publications/oregon-residents-struggle-afford-high-healthcare-costs-covid-fears-add-support-range-government-solutions-across-party-lines.

- Oregon Legislative Information, 2021 Regular Session: HB 2010 B, accessed 21 July 2021, archived at https://web.archive.org/web/20210721231855/https://olis.oregonlegislature.gov/liz/2021R1/Measures/Overview/HB2010.

- Chiquita Brooks-LaSure et al., Manatt, Oregon Public Option Report: An Evaluation and Comparison of Proposed Delivery Models, December 2020, p. 8, archived at https://web.archive.org/web/20201218153709/https://www.oregon.gov/oha/HPA/HP/docs/Manatt-Health-Oregon-Public-Option-Report-An-Evaluation-of-Proposed-Delivery-Models-December-16-2020.pdf; Matthew Fiedler, Brookings Schaeffer Initiative for Health Policy, Capping Prices or Creating a Public Option: How Would They Change What we Pay for Health Care?, 19 November 2020, archived at https://web.archive.org/web/20210415020543/https://www.brookings.edu/research/capping-prices-or-creating-a-public-option-how-would-they-change-what-we-pay-for-health-care/.

- Oregon Health Authority, Office of Health Policy, Sustainable Health Care Cost Growth Target, accessed 11 June 2021, archived at https://web.archive.org/web/20210523121940/https://www.oregon.gov/oha/HPA/HP/Pages/Sustainable-Health-Care-Cost-Growth-Target.aspx.