Earlier this week, USPIRG Education Fund released "Big Banks, Big Complaints," a report documenting how the CFPB is helping bank customers with its public complaint database. Today, the CFPB announced it had imposed a $20 million civil penalty on JP Morgan Chase and ordered it to refund $309 million to over 2 million consumers for deceptively marketing junky credit card add-on products, some of which consumers didn't even receive. The CFPB is getting results.

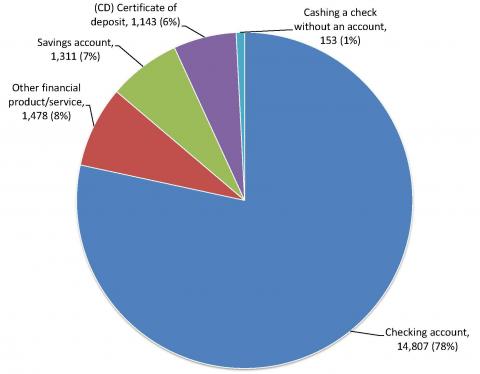

Earlier this week, USPIRG Education Fund released “Big Banks, Big Complaints,” a report documenting how the Consumer Financial Protection Bureau (CFPB) is helping bank customers solve disputes through its searchable public online complaint database. Here’s a screenshot from the report.

Today, the CFPB announced it had imposed a $20 million civil penalty on JP Morgan Chase and ordered it to refund $309 million to over 2 million consumers for deceptively marketing junky credit card add-on products, some of which consumers didn’t even receive. (The Office of the Comptroller of the Currency (OCC), Chase’s previous consumer regulator, also added a $60 million penalty.)

Without a doubt, the CFPB is getting results. “At the core of our mission is a duty to identify and root out unfair, deceptive, and abusive practices in financial markets that harm consumers,” said CFPB Director Richard Cordray.

Both the complaint database and the Chase enforcement action are right at the core of that CFPB mission. The enforcement action stopped an unfair practice, refunded money to those harmed and sent a stern warning to other banks that the CFPB is on the bank crime beat.

And as my colleague Laura Murray explained in the news release accompanying our report:

“Thanks to the CFPB’s complaints database, consumers who get ripped off or misled by their banks can make their voices heard and get satisfaction,” said Laura Murray, Consumer Associate for the US PIRG Education Fund. “Other consumers can view the public database and make smarter, more informed financial choices. By providing a roadmap for navigating the tricks and traps of the financial marketplace, this database is another way the CFPB gets real results for consumers.”

Companies that behave better in the marketplace by handling complaints quickly or eliminating unfair practices should be rewarded. Consumers will see fewer complaints about them and migrate their accounts to get better services. Firms that persist in unfair practices may make money in the short run, but ultimately, transparency will help better actors.

Our first report on the CFPB complaint database took a deep dive into bank account complaints. Future reports in the series will look at complaints about student loans, credit bureau errors and credit cards. I just took a quick look at the CFPB’s searchable complaint database. I looked at “credit card” complaints and filtered for the issue “credit card protection/debt protection.” That’s the category that includes complaints about “add-on” products. As of today, the CFPB has received 888 complaints about add-on products. Hint: They weren’t all about Chase. In fact, in 2012, the CFPB went after Discover and Capital One credit cards for deceptive sales of similar products.

What should consumers do now?

Finally, today’s CFPB/OCC enforcement action against Chase was announced the same day as investor and safety regulators hit Chase with a total of $920 million dollars in penalties over its $6 Billion “London Whale” derivatives trading debacle. These, and the CFPB settlement, are all good settlements for consumers and investors, but U.S. PIRG continues to point out that they would be even better if the settlements were worded to prohibit wrongdoers from taking a tax write-off. Wrongdoer penalties should not be a cost of doing business, they should be a punishment and a deterrent.

Senior Director, Federal Consumer Program, U.S. PIRG Education Fund

Ed oversees U.S. PIRG’s federal consumer program, helping to lead national efforts to improve consumer credit reporting laws, identity theft protections, product safety regulations and more. Ed is co-founder and continuing leader of the coalition, Americans For Financial Reform, which fought for the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, including as its centerpiece the Consumer Financial Protection Bureau. He was awarded the Consumer Federation of America's Esther Peterson Consumer Service Award in 2006, Privacy International's Brandeis Award in 2003, and numerous annual "Top Lobbyist" awards from The Hill and other outlets. Ed lives in Virginia, and on weekends he enjoys biking with friends on the many local bicycle trails.