UPDATED: Added House Floor Letter Opposing HR 10, Wrong Choice Act, Link: Yesterday we released a report showing how the CFPB works to protect servicemembers, veterans and their families from financial predators that “line up outside our military bases like bears on a trout stream.” Today the House begins floor debate on the so-called Financial Choice Act. This Wrong Choice Act, incredibly, turns the CFPB into an unrecognizable husk incapable of protecting anyone, including servicemembers.

UPDATE: Link to our letter to all Representatives opposing the Wrong Choice Act.

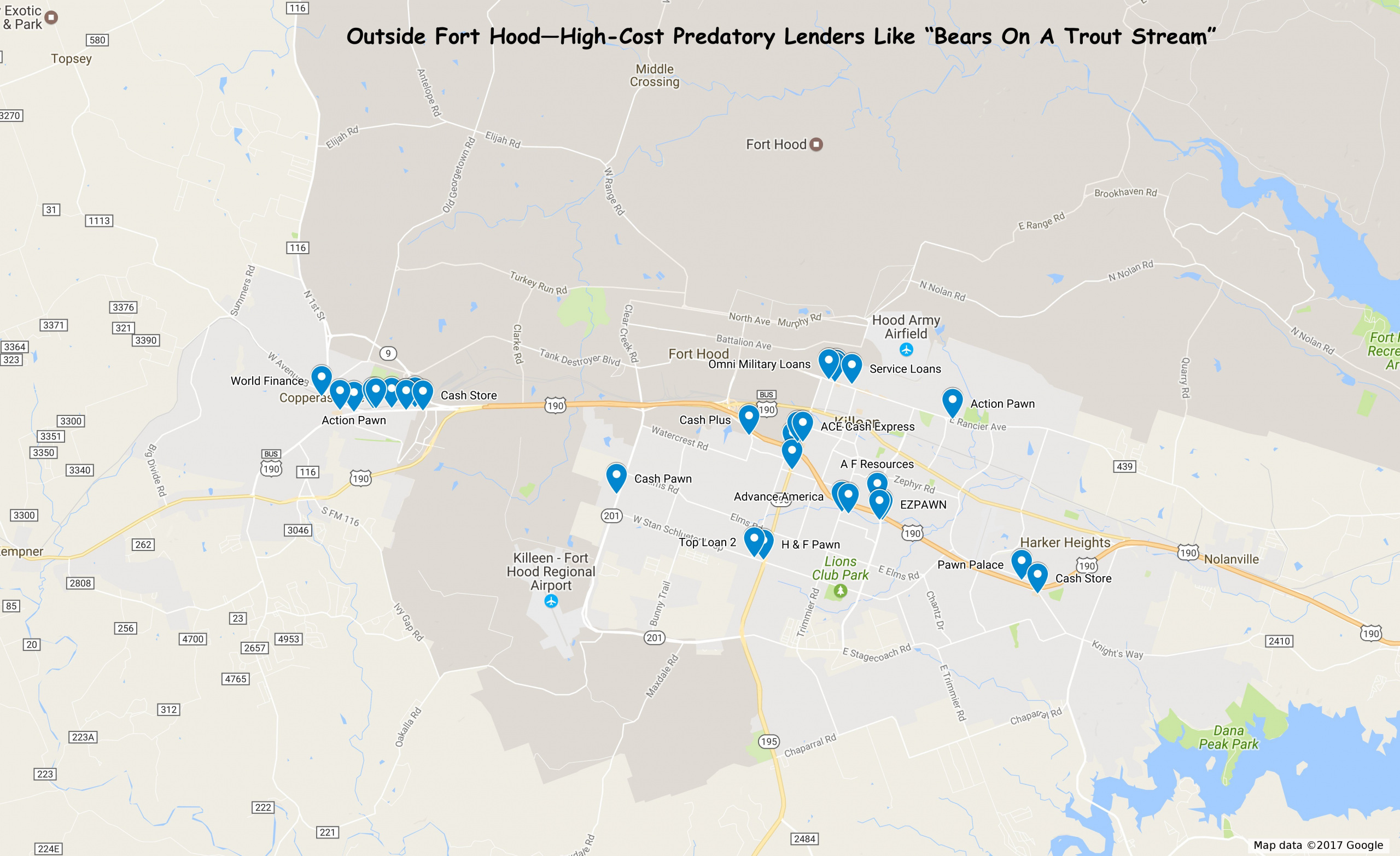

Original Post: Yesterday we released the U.S. PIRG Education Fund/Frontier Group report “Protecting Those Who Serve,” showing how the CFPB works to protect servicemembers, veterans and their families from financial predators that “line up outside our military bases like bears on a trout stream.” Chart is a google map of predatory lenders outside approaches to Fort Hood, Texas. Today the House begins floor debate on the so-called Financial Choice Act (our detailed opposition letter). This Wrong Choice Act, incredibly, turns the CFPB into an unrecognizable husk incapable of protecting anyone, including servicemembers.

The report is the 10th report in a series of ours based on analysis of complaints in the CFPB’s Public Consumer Complaint Database. We looked at 44,000 complaints with “military” tags. The report goes onto explain how financial problems from either predatory lending, unfair practices or credit bureau mistakes affect military family lives and affect the nation’s unit preparedness. Unit preparedness? According to the Pentagon, bad credit is the leading cause of servicemembers losing security clearances, severely affecting our ability to field and deploy an adequate force to defend the country.

We were privileged to join several military support organizations that support the CFPB to help release the report at the Veterans of Foreign Wars (VFW) national headquarters. At left, John Towles, deputy legislative director for the VFW, discusses the CFPB and the report. (I am at left and Mike Litt of U.S. PIRG is at right; in addition to VFW officials, Michael Saunders, Deputy Legislative Director of the Retired Enlisted Association is 4th from left and William Hubbard, Vice President of Government Affairs, Student Veterans of America is behind John Towles in red shirt. Other military organizations commenting on the CFPB and servicemembers include Veterans Education Success and the National Military Family Association, as seen in our release. Photo: Suzannah Hoover Photography)

The design of the Financial Choice Act is diabolical. The bill eliminates the CFPB’s independent agency status and its independent funding; placing it in the executive branch and under the highly-politicized appropriations funding process. It also eliminates most of its funding anyway and sets it up for further appropriations cuts or limits on what it can do with whatever money is left.

It then takes away nearly all of CFPB’s enforcement, marketplace surveillance and rulemaking tools.

Without virtually any funding, or any enforcement and marketplace surveillance tools, the CFPB will be hard-pressed to identify illegal acts under or enforce any of the laws, including the Military Lending Act and the Servicemembers Civil Relief Act, providing special protections for servicemembers and veterans. Of course, this rollback also applies to other laws that protect servicemembers and everyone else, including the Truth in Lending Act, the Fair Credit Reporting Act, the Fair Debt Collection and Practices Act and other laws.

Of course, the above attacks on the CFPB hinder its ability to protect any consumers, including servicemembers. Finally, though, as a kicker, the Financial Choice Act also makes the CFPB’s statutory Office of Servicemember Affairs into an “optional” office, meaning a future director could eliminate it. To learn more about what the OSA does, see page 15 of the report “Protecting Those Who Serve.” (The bill also makes CFPB offices for students and older Americans optional).

The Wrong Choice Act Sets On A Road to Further Economic Collapses

Our detailed letter opposing HR 10, the so-called Financial Choice Act, also details its many weakenings to other aspects of the 2010 Dodd-Frank Wall Street Reform and Consumer Protection Act. The Dodd-Frank Act gave prudential regulators including the Federal Reserve and FDIC additional powers to watchdog banks and other financial players to prevent the dangerous practices that caused the financial collapse of 2008 and led to the great recession. It established a new Financial Stability Oversight Council to ride herd over very large, complex institutions whose actions or failures could impact our financial system. It gave the tiny Commodities Futures Trading Commission and Securities and Exchange Commission more authority to watch over reckless trading in derivatives and other investment instruments.

That second-worst financial collapse, which only caused millions to lose homes, millions more to lose jobs and millions more to lose trillions in retirement savings happened less than ten years ago. Have proponents of the Financial Choice Act forgotten it, or do they choose to ignore it at our peril? Either way, HR 10 is the wrong choice, a cruel choice and a dangerous choice. Its proponents reject consumer protection, they reject protecting those who serve from financial predators, and they reject their responsibilities as stewards of the nation’s government and its financial system.

Senior Director, Federal Consumer Program, PIRG

Ed oversees U.S. PIRG’s federal consumer program, helping to lead national efforts to improve consumer credit reporting laws, identity theft protections, product safety regulations and more. Ed is co-founder and continuing leader of the coalition, Americans For Financial Reform, which fought for the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, including as its centerpiece the Consumer Financial Protection Bureau. He was awarded the Consumer Federation of America's Esther Peterson Consumer Service Award in 2006, Privacy International's Brandeis Award in 2003, and numerous annual "Top Lobbyist" awards from The Hill and other outlets. Ed lives in Virginia, and on weekends he enjoys biking with friends on the many local bicycle trails.